Stagflation or Recession? The Data Points to Neither

Despite a loud chorus of market voices forecasting either stagflation or a looming recession, the U.S. economy is exhibiting none of the key markers associated with either condition. A deep dive into macroeconomic indicators from GDP and inflation to labor and credit shows a more nuanced reality: a resilient economy in a late-cycle normalization, not one on the brink of collapse.

The Narrative Trap

Both stagflation and recession have become narrative crutches. Sticky service inflation, hawkish Fed messaging, and equity market volatility have all contributed to a climate of pessimism. Market analogies to the 1970s or post-hiking cycle slowdowns are common. But the data simply doesn't corroborate this narrative.

Growth: Positive, Not Contractionary

Real GDP continue to affirm a trajectory of moderate but sustained economic growth in the United States. Despite a deceleration from the elevated post-pandemic growth rates observed in 2021–2023, the economy has not entered contractionary territory. Year-over-year GDP remains solidly positive, and quarterly prints have consistently avoided back-to-back declines disqualifying the presence of a technical recession by standard definitions.

An analysis of long-term GDP, overlaid with NBER recession periods, reveals no emerging pattern consistent with historical recessions. Past contraction phases were marked by sharp and persistent negative growth, often coinciding with systemic shocks (the 2008 financial crisis or the COVID-19 pandemic in 2020). In contrast, the current environment is characterized by:

Resilient household consumption supported by labor market strength (wage and employment stability).

Stable corporate investment, bolstered by structural policy support ( industrial policy, infrastructure investment).

Improving external demand, partially offsetting tighter domestic financial conditions.

Importantly, the real economy has proven more robust than suggested by leading sentiment surveys or market narratives that oscillate between fears of hard landing and stagflation. While growth has normalized from its cyclical highs, macro fundamentals do not currently support scenarios of stagflation defined by persistent inflation coexisting with stagnant or negative growth nor do they align with a contractionary cycle.

In summary, the current U.S. economic backdrop is better described as a transition from peak post-pandemic growth toward a more sustainable expansion phase. Forward-looking risks remain particularly around monetary policy lags and geopolitical volatility but the available data offer no empirical basis to suggest the U.S. economy is entering either a recession or a stagflationary regime

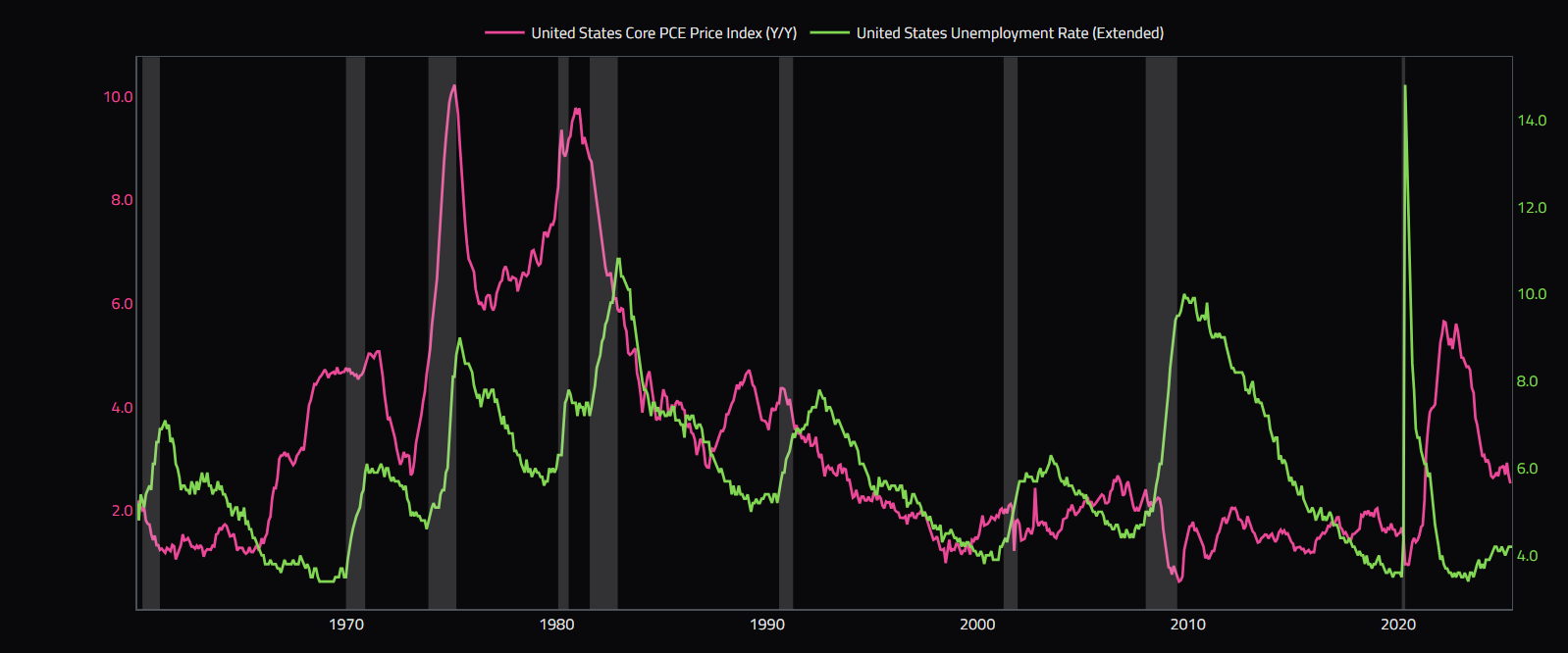

Labor Market: Softening, Not Breaking

Despite prior inflationary pressures, the Core PCE has steadily declined, and unemployment remains historically low, around 4%. This contrasts sharply with stagflation periods of the 1970s–80s, which featured both elevated inflation and high joblessness.

Labor market strength remains intact layoffs are limited, and wage growth is moderating, reducing fears of a wage-price spiral.

Inflation is cooling, particularly core inflation, which is approaching the Fed’s long-term target.

Both jobs and inflation are moving in a direction consistent with a soft landing, not a recession or stagflation.

The data show that concerns about stagflation are not supported by current economic fundamentals, but rather stem from speculative narratives disconnected from the underlying trends.

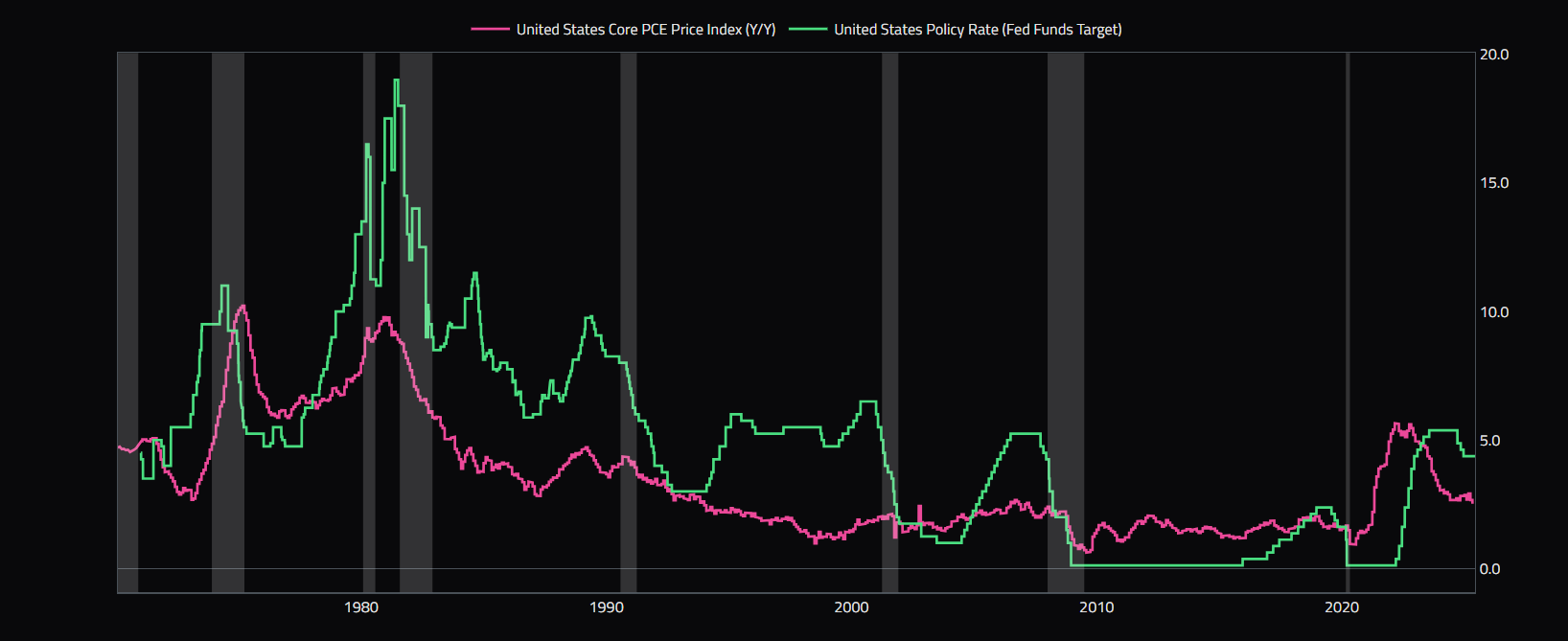

Inflation: Cooling Along the Right Path

Core PCE, the Fed’s preferred measure, has been steadily declining over the past 18 months, indicating a clear disinflationary trend. The 3-month annualized Core PCE is approaching the Fed's 2% target, reinforcing the view that inflationary pressures are easing. Despite occasional bumps in headline inflation, expectations remain anchored in both consumer surveys and market indicators. This dynamic contradicts any stagflation narrative rather than rising inflation amid stagnation, inflation is falling while economic growth persists.

Credit: Healthy and Contained

Current credit market conditions show no signs of systemic stress typically seen before recessions. High-yield credit spreads are stable, elevated versus 2021–22 but flat over the past six months and consumer delinquencies, while rising modestly, remain historically low. The absence of a sharp spike in either metric suggests a normalization phase rather than panic. Lending activity remains cautious but intact, and bank capital positions are strong, pointing to a resilient and functioning financial system rather than one under strain.

Pricing in a Risk That Hasn’t Materialized

Much of the recession/stagflation fear appears to be driven by positioning, not fundamentals. Investors remain heavily exposed to duration, gold, defensives, and low-volatility equities. These trades imply fear yet data suggests stabilization.

This creates a narrative dislocation: the positioning is priced for risk, but the data isn’t validating that risk yet. That mismatch presents opportunity.

Risks to Monitor

As Chair Powell often emphasizes, this analysis remains data-dependent. Key risks could still bend the current trajectory, and this week’s inflation data will be critical in assessing whether there’s any material deviation from the disinflationary path toward the Fed’s target.

Sticky services inflation, particularly in shelter and insurance

Energy price shocks, amid heightened geopolitical tensions

Lagged monetary policy impact

Global drag from China and Eurozone weakness

However, these are watchpoints, not foregone conclusions.

Conclusion: Gradual Normalization Continues

The U.S. economy is cooling in a controlled fashion. Growth is slowing, not contracting. Inflation is falling, not accelerating. And labor markets are moderating, not collapsing.

This is not 1970s stagflation. It’s not 2008. It’s not even 2020. It's 2025, a late-cycle economy digesting tight monetary policy, still supported by consumption, capex, and improving real incomes.

Unless the data materially changes, the louder macro risk may not be recession or stagflation but mispriced optimism on markets overestimating how much the Fed needs to do from here.